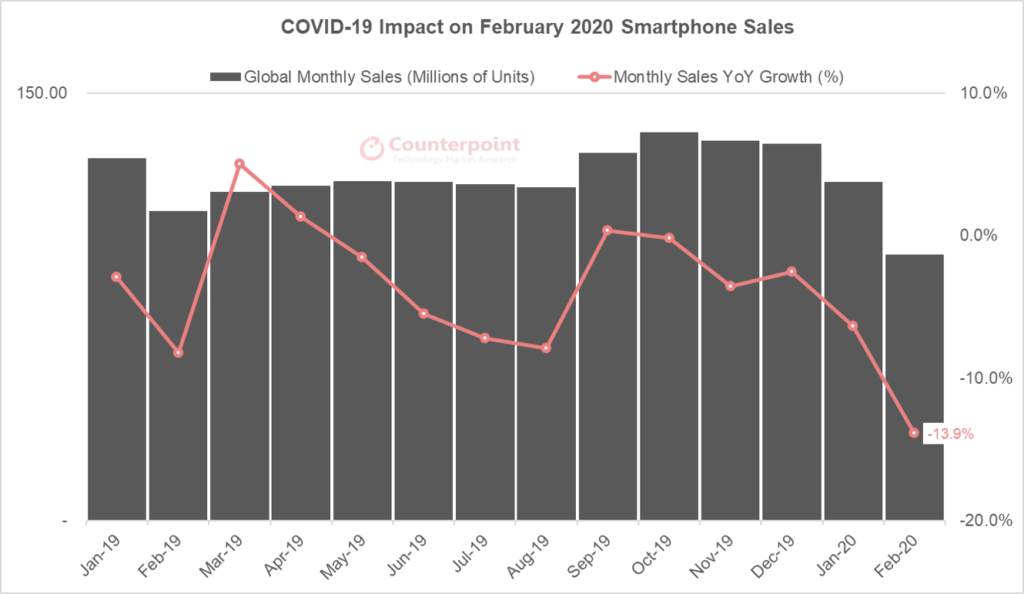

As COVID-19 takes its toll, market demand is fragile but global smartphone sales (sell-through) in February declined only 14% compared to last year, showing some resilience. From the supply-side, global smartphone shipments (sell-in) fell a slightly more, down 18% compared to last year, but again a lower than expected drop.

As COVID-19, unfortunately, spreads like wildfire around the globe, its impact on the technology industry is unprecedented. The global February smartphone sales, as a result, showed weakness, but the decline was no more than 14% lower than February 2019; not as bad as the industry had feared.

However China, the initial epicenter of the epidemic, did show a huge 38% decline, but is showing signs of a rebound already. Overall, global smartphone sales in February showed weakness in many markets as consumers became cautious. But with the growth of online channels, we saw sales shifting from offline to online. Offline sales in China fell more than 50% during February. But this fall was partially offset with stronger online sales, so the overall drop at 38%, was not so severe.

Sell-in shipments, which represents the supply of smartphones, were relatively weaker, but February is a traditional low period for production, especially if it coincides with the Chinese New Year as was the case this year. Comparing with a year ago, sell-in shipments fell 18%, though again, less bad than the industry feared.

VP and Research Director, Peter Richardson, commenting on the smartphone demand-supply landscape and outlook, “The global smartphone market is largely a replacement market, meaning that smartphones are a discretionary purchase. Nevertheless, they are now seen as a vital part of daily life – especially so for those enduring extended periods of isolation or remote working.

So while people may delay purchasing due to the coronavirus pandemic, especially in the early part of the crisis when the disruption and uncertainty are both high, they will still replace their smartphone at some point. This means that sales will not be entirely lost – just delayed.”

In terms of the competitive landscape, the demand for Samsung smartphones remained stable due to the minimum exposure to the Chinese supply chain and China market demand, thus, capturing 22% global smartphone market share in terms of sales volumes. Apple felt some impact from the supply-side during the month both in China in early February and outside of China in the latter half of the month which affected its sales performance.

However, Huawei which has maximum exposure to China from both supply and demand perspectives, actually performed well above expectations, selling more than 12 million smartphones during February, seeing just a 1% drop in global market share.

Jene Park, Senior Analyst at Counterpoint, commenting on the impact outside China, noted, “While China and South Korea are gradually recovering, the worst is far from over for many other parts of the world. The coronavirus pandemic is unprecedented in nature and scale, but there are historical parallels we can learn from and these give us confidence that the mobile communications sector can ride-out this storm without too much damage in the longer term.”