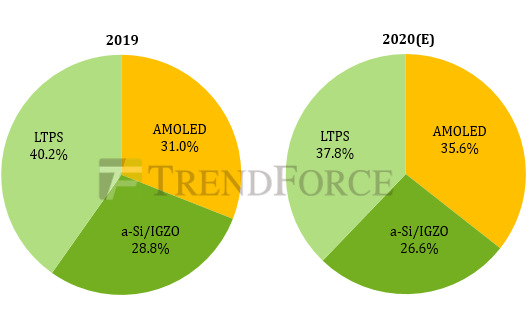

According to the latest observation of WitsView, global smartphone production has scaled down due to the COVID-19. It affects the proportion of panels adopting different display technologies. Since mobile phone brand customers are still adopting AMOLED panels, it is expected that the penetration rate of AMOLED models will increase from 31.0% in 2019 to 35.6% in 2020. While the penetration rate of TFT-LCD models, whether LTPS panels or a-Si panels, will decline.

The influence of Chinese panel manufacturers is increasing. And the proportion of AMOLED production capacity will increase to 35% in 2020.

Fan Boyu, the assistant manager of WitsView, points out that flagship model plans of most of the mobile phone brand customers will be mainly done based on AMOLED panels in 2020. Including the new models that will announce by Apple in the second half of the year.

Although the penetration rate has been revised down from 37.7% to 35.6% which is still higher than the 31.0% in 2019. The new production capacity of AMOLED panels is increasing, especially that from Chinese panel factories are increasing significantly. It is expected that the proportion of the global production capacity will jump from 26% in 2019 to 35% in 2020.

The Chinese panel factories are bound to make an increase in use and product yield. They are active penetrating the supply chain of first-tier brand customers as their goals. They will continue to expand their influence.

The production capacity expansion of LTPS panels slowed down, and their supply was relatively stable in the past two years. However, due to the great price competition and the good performance in the field of narrow bezels and power-saving specifications, the LTPS panels have become the mainstream in the smartphone market.

This drives the a-Si panels back to the low-end market. As a significant increase in the supply capacity of AMOLED panels, the market share of LTPS panels in the mid-to-high-end market has encroached. With the gradual fermenting of the impact in the mobile phone market caused by the epidemic, those smartphone brand customers prefer to prolong the sales cycle of old models or maintain or even expand the number of low-end models.

All these are not conducive to maintaining the penetration rate of LTPS models in the mid-range market. It is expected that the penetration rate of LTPS models will decline from 40.2% in 2019 to 37.8% in 2020; a-Si models will decline from 28.8% in 2019 to 26.6%. The decline of LTPS models will be slightly greater than a-Si models.

In the long run, AMOLED models will continue to expand the market scale and become the mainstream of the smartphone market. Meanwhile, TFT-LCD models, including both LTPS and a-Si, will decline gradually.

The LTPS panel factories that made mobile phones as their main production capacity are bound to look for other outlets. For example, panels for notebooks, tablets, automobiles, etc., so that to support their use of production capacity.